Auditing,

Forecasting, and Market Research

How They Work Together

The triad of auditing,

forecasting and market research are usually thought of as only attainable using

sophisticated AI software algorithms and technology. The goal of Auditmetrics

is to show that data science does not start with technology but how one

approaches business data analytics with an understanding of the fundamental

principles of statistical analysis.

Auditing, Forecasting, and Market Research

three components are

interconnected in several ways:

1. Data Integrity: Auditing ensures

that the data used in forecasting is accurate and reliable. By verifying the

quality of data sources through audits, organizations can improve the accuracy

of their forecasts. For instance, if an audit reveals inconsistencies in the

administration of sales data collection methods, adjustments can be made to

enhance future forecasting efforts.

2. Revenue Trends:

Forecasting

helps managers guide strategy and make informed decisions about critical business

operations such as sales, expenses, revenue, and resource allocation. Forecasting

adds a competitive advantage and can be the difference between successful and

unsuccessful outcomes. Another benefit is that financial institutions will not

put money in a business if it’s unable to provide a set of thoughtful forecasts.

financial forecasts will also help develop operational and staffing plans that

will make a business more efficient.

3. Informed Decision Making: Market research

provides valuable insights that can guide both auditing processes and

forecasting models. By understanding consumer behavior and market dynamics

through research, organizations can set realistic goals during audits and

create more accurate forecasts that reflect current market conditions.

Continuous

Improvement:

The feedback loop created by these three components fosters continuous

improvement. Audits can identify gaps that can impact forecasting accuracy and

impede meaningful market research methodologies. The audit corrects latent data

issue which can lead to improved forecasting techniques which in turn can lead

to better-informed market research initiatives that align with organizational

goals.

Bringing it Together

In

this section we will go over the transition from the audit to the forecast

using a sample created by the Auditmetrics AI.

1. Data

Integrity

The audit is the

starting point to assure that cashflow is performing with efficiency. A random

sample is of upmost importance in conducting a valid audit. We will not go in

to detail on this step. That is better handled in the “Getting Started”

documentation.

Suppose a fiscal

manager wants to do an audit of a sales account with a million transactions.

The AI process guides the manager to obtain an Excel statistical sample that

can vary from 400 to 1000 records depending on the chosen precision, or as the

pollsters term it “margin of error”. The AI process conforms to AICPA and IRS

standards.

It would be valuable

to review the case studies in chapter 2. Chapter 4 goes into more technical

detail about the issue of statistical efficiency in the context of the sales

tax audit. Spending time to understand statistical efficiency is well worth the

effort (pp. 25,37,41-45,127). It is the pervasive underlying corner stone of

all statistical inference processes for such diverse disciplines as medicine,

economics, physics, biology, opinion polling and other social sciences. Take

the time to understand it rather than pass it on to AI alone to do the thinking.

2. Revenue

Trends

Transition data from audit

to Forecast

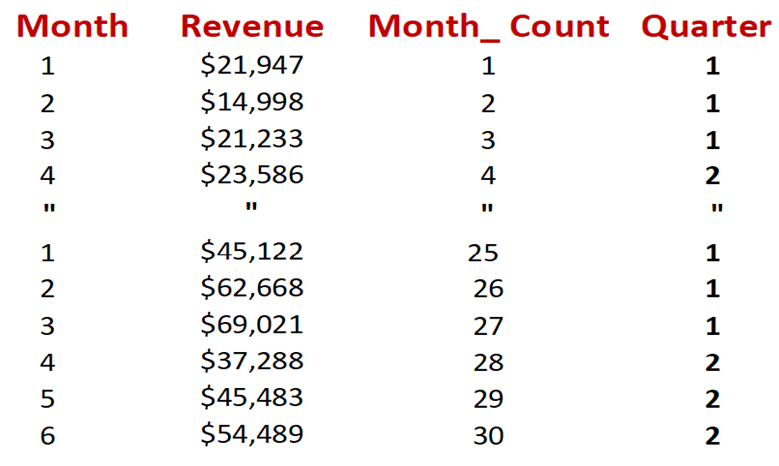

Table 1 – Auditmetrics

generated Random Sample that was used for an audit

Table

1 is a condensed exhibit of the sample (n= 1,158) using a 3% margin of error.

In preparing the sample for forecasting two new variables are added. For first

row the new cells are:

Year - Excel function:

=Year(C2)

Month- Excel function:

=Month(C2)

The Excel sample

represents 30 months of data over a 2 ½ year period. It is sorted by Year and

Month by going to “Data” on the top menu and select “Sort”. In the exhibit are

the sort inputs:

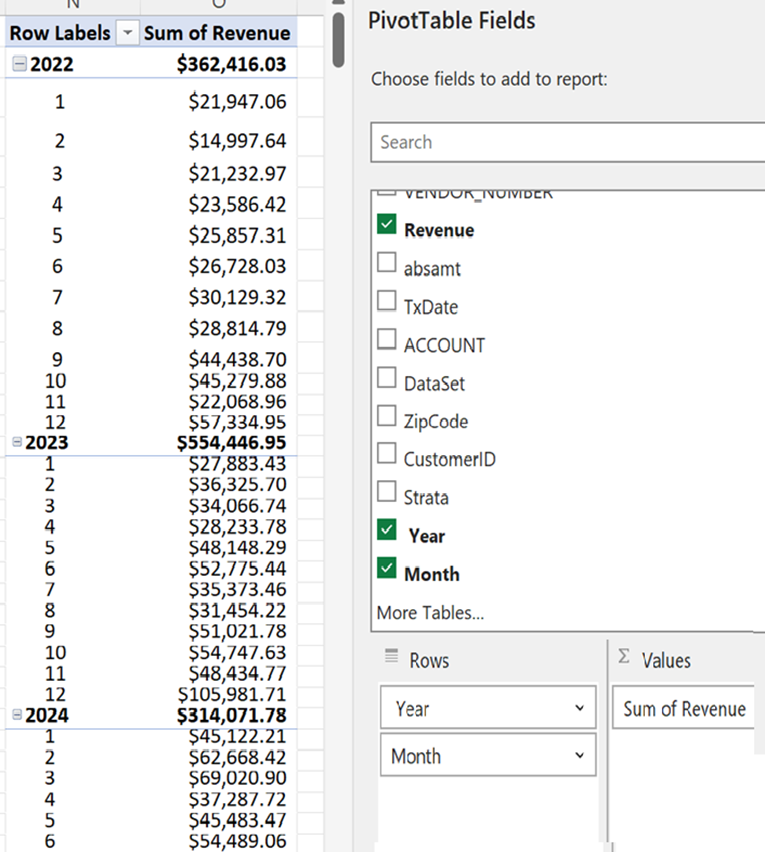

The next

step is to create a summary dataset that lists total revenue by month for the 2

½ years. The Excel tool is the Pivot Table. Select the dataset of interest and then

select insert and then Pivot Table.

Figure 1-

The pivot table set up and results

The

resulting data table can now be used for a 30 month forecast

of revenue. Table 2 is a restructuring of the data for using regression to

create a prediction model.

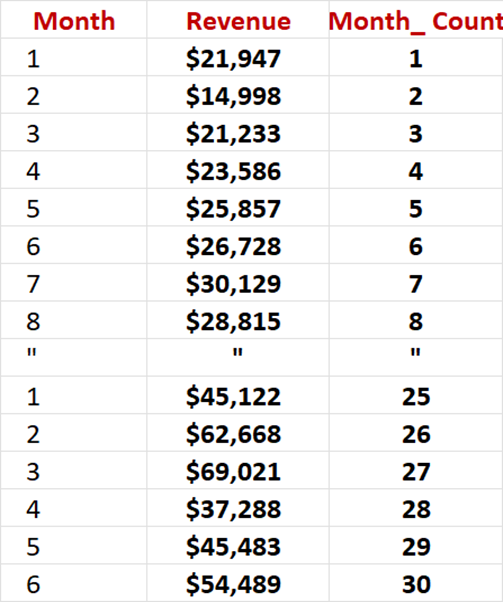

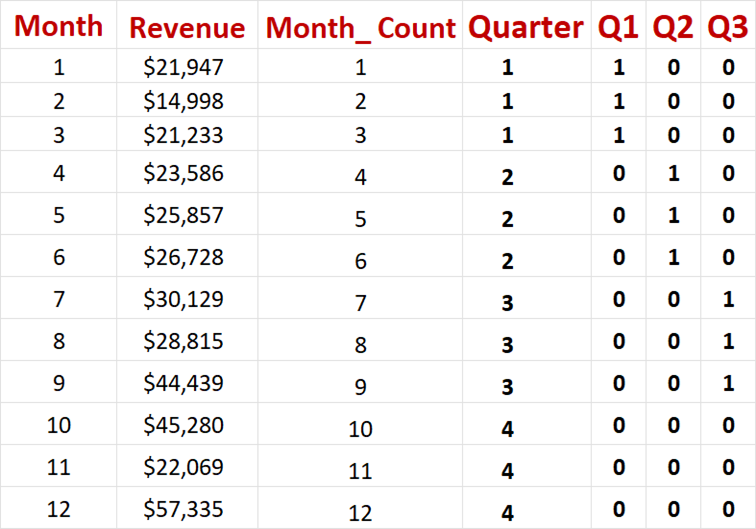

Table 2 –

Dataset for Regression Predictions

What

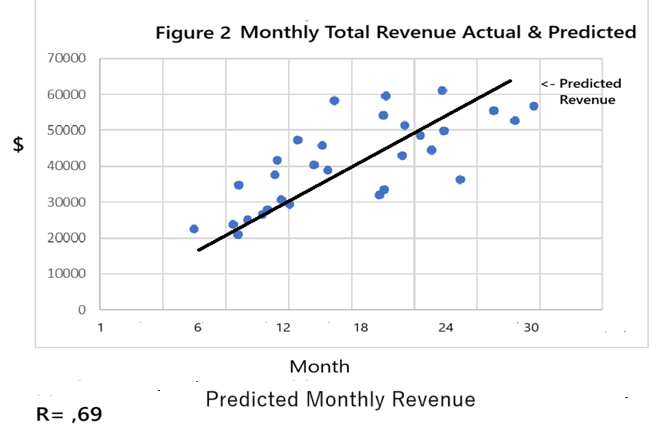

is added is a new variable “Month_Count”. Does

Revenue increase as we go from Month 1 to month 30?

Monthly

Sales =$19,350 + ($1,412

x Month_Count)

A

full discussion of regression modeling is in Springer Appendix I pp. 107-111.

The details of how to use Excel’s ToolPak for

Regression is on pp. 60-67.

Unfortunately,

this regression model is not complete. So far, the basic model is a bivariate

linear model, a dependent variable with only one predictor variable. Though we

have a very good fit, there is a problem with the model.

The data is

that of a wholesaler that supplies retail outlets. With this prediction model

the next month will always be higher than the previous month. But business

activity does have seasonal fluctuations. The fourth quarter of the year and

its holiday activity will always be higher than the following first quarter of

the following year. The model as it exists does not allow for seasonal

fluctuations.

We need a

new multiple regression model with two predictor variable types to perform

monthly and quarterly adjustments. It is a statistical technique that uses several

explanatory variables to predict the outcome of a dependent variable. In essence,

multiple regression is an extension of our current regression model sometimes

referred to as bivariate regression. Multiple regression involves more than one

explanatory variable. in the new forecasting

model are added quarterly variable inputs to the pivot table. The model will

now conduct forecasts that adjust for seasonal fluctuations.

Table 5 –

Quarterly Variable Added

Table 5 adds

the quarterly value for each month. Jan Feb March are all the first quarter of

the year. Month 4 or April starts the second quarter.

The multiple

regression dataset below takes into account seasonal fluctuations.

Table 6 –

First Year Dataset with Quarterly Variables

The

rationale and details of introducing the quarterly adjustment variables (Q1,Q2,Q3) is on pp 64-67 in the Springer Book.

The

model as reported by toolpak is:

|

|

Coefficients |

|

Intercept |

28404.26 |

|

Month_ Count |

1210.023 |

|

Q1 |

-8315.13 |

|

Q2 |

-10909.1 |

|

Q3 |

-8472.54 |

This model

has a correlation of R =.78 which

indicates a marked improvement of the model. It would be very useful to review

again Appendix I pp 107-111 regarding the concept of goodness of fit of

the model.

The

following discussion is excerpted from the Springer book. It deals with some

methods of market research that can be readily implemented by small businesses.

3.

Informed Decision-Making

Regression

and Local Market Area -Regression is very valuable in adjusting predictions

using categorical adjustments for various demographics factors such as

geographic region and other characteristics such as gender. Geographic region

can also be a surrogate for income distribution which is readily available from

government published data. For example, there is available through census data

sources that break down income tax collections or median income by zip code.

Such geographic data combined with a company’s sales data with zip codes from

its account record is an indicator of socioeconomic characteristics of a

business’ customer base.

The compilation of this

type of socioeconomic dataset requires time, but gaining insight of the

customer base is invaluable. The first step is to set up a dataset of sales

accounts that include customer zip code.

The first step is to group zip codes into

broader zip code areas. This is where background research of examining census

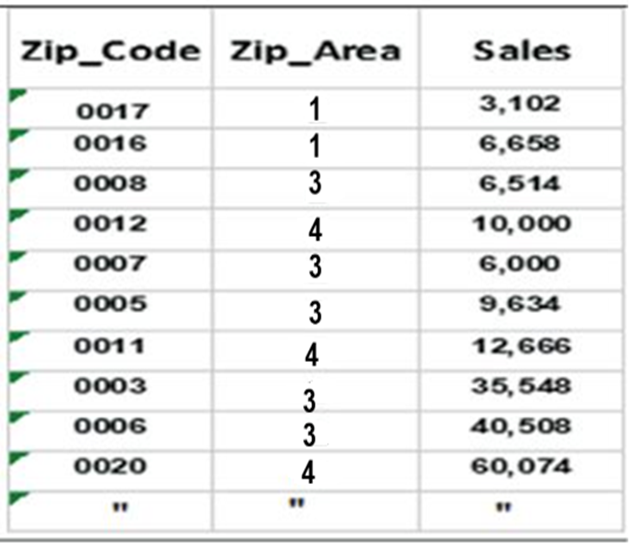

data to develop sociodemographic relevant zip code areas (Table 8.1).

Table 8.1 sales and

sociodemographic research resulted in condensing the data into four geographic

areas. This number was chosen to simplify the presentation of the concept of

using regression to project sales by geographic area. It is most likely that

many more areas would be of value, especially for larger businesses. From a

statistical data perspective, zip codes are categorical data.

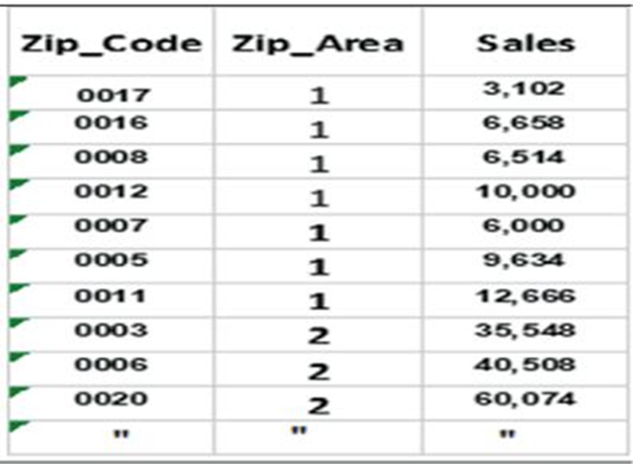

Table 8.1 Sales Data by Zip

Code and by Four Geographic Areas

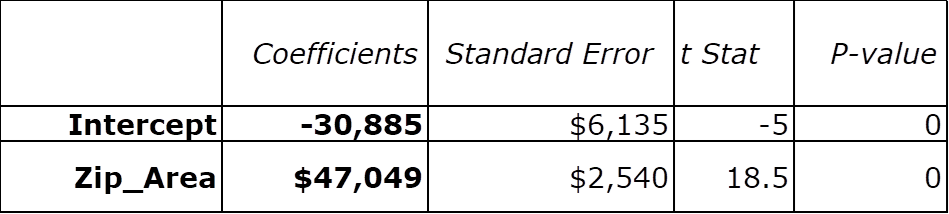

Regression results:

R=.86

R2=.74

Sales = -$30,885 + $47,049 x Zip (Geographic Area number)

Pivot table to summarize

sales by zip code area

As part of small business forecasting,

it is key to get a picture of the possibilities for selling products or

services in a local market. Looking at local markets will provide information

about the types of individuals who might buy products or services and how

extensive is the company’s geographic reach and what is the competition within

the various market areas.

Create a

Customer Profile Next there is a need to

determine who are the people who will buy products or services.

at what

age are they?

What

is their income level?

What

is their education level?

What

kind of jobs do they have?

What do they like to do

for entertainment?

It may be too cumbersome

and difficult for a small business to survey for such data. But a small

demographically diverse focus group is a proven way to measure customer

opinions. It is set up in guided or open discussions about new products or

current views of the company to determine reactions that can be expected from a

larger population. The use of focus groups is a market research method that is

intended to collect data through interactive and directed discussions by an

experienced interviewer. If there are issues with lagging sales that don’t

respond to standard means of marketing, then arranging for a focus group may

be what is needed.

Springer book pp. 81-86 discusses how

to coordinate opinion Likert data with regression projections.

Constant

Monitoring of Business Activities

Regular timely random samples allow the

business manager to deal with small workable subsets of account data

representative of the total book. There is no need to use the gold standard of

3% margin of error with its sample size of 1,152 which should be reserved for

official filings such as for tax agencies or fiscal year end assessments and

reporting.

Regular

routinely smaller samples in the 5% to 7%. range would require samples

approximately 40% smaller reducing cost. Despite the reduced precision of a

single point in time individual estimate, the random process trend over time

will provide a fairly steady indication of trends.

Total Process Overview The overall process in conducting forecasting and market

research is to:

1.

Start with a random sample of

accounts.

2.

From there use regression to project

revenue and expenses.

3.

Also add to the account data pertinent

variables such as geographic and socio-demographic data.

4.

Set up a mechanism to obtain customer

ratings using Likert scales.

5.

The total process from audit to market

research cannot be done without also being closely connected to the personnel

and operations of the business. The major benefit is creating an environment leading

to technology and employee cohesion.

Conclusion: A Synergistic Approach

In conclusion, auditing, forecasting,

and market research work together synergistically to enhance organizational

effectiveness. Ensuring data integrity through audits leads to confidence in the

insights from forecasts and market research.

informed decision-making results in utilizing accurate forecasts for

strategic planning. As a result businesses can achieve greater success in their

operations.

Other Auditmetrics Resources

Auditmetrics Small

Business Power Series books available on Amazon:

Both Kindle and Paper Bound Available

Statistical Audit

Automation

Applying

Artificial Intelligence Techniques

Forecasting Revenue and Expenses for Small

Business Using Statistical Analytics

Market Research for Small

Business

Using Statistical

Analytics

Value Added in Healthcare

and Public Health

Value added is the

extra value created over and above the original value of something

• For private business it is usually the

products sold to the consumer

• It

is the difference between a product final selling price and the direct and

indirect

expenses incurred in providing that product

In healthcare and

public health, the challenge is how to measure value added

•Research into organizations that have

achieved better health outcomes while often

lowering costs suggests a strategic framework

for value-based public health and

healthcare

implementation

•Focusing on health outcomes aligns how

patients experience their health with links to

the investment

incurred

•This

is the basis of cost effectiveness and cost benefit analysis of public health

and

healthcare programs

Also available on Amazon:

HealthLink Wellness: Science for the

Individual